📢Attention:Small Business Owners, Established Entrepreneurs, & Future Dream Builders

The game isn’t about credit scores. The game is about credit positioning.

How I Built a Credit Profile That Unlocks $20K–$100K+ in Personal & Business Funding

For years, I did what everyone else was told to do. Pay on time. Keep utilization low. Watch my credit score.

Only ($97) $17 Today - $50 OFF

(Save $80.00 today)

Get The Are Fundable Ebook Now + Receive Instant

Access to Bank Ready Ebook For FREE

No Shipping. No Waiting. Instant Access.

100% Secure Checkout

banks and business lenders offering low-doc, minimal

documentation funding opportunities to help you grow.

Here’s What Most People Don’t Understand And Why They Stay Stuck

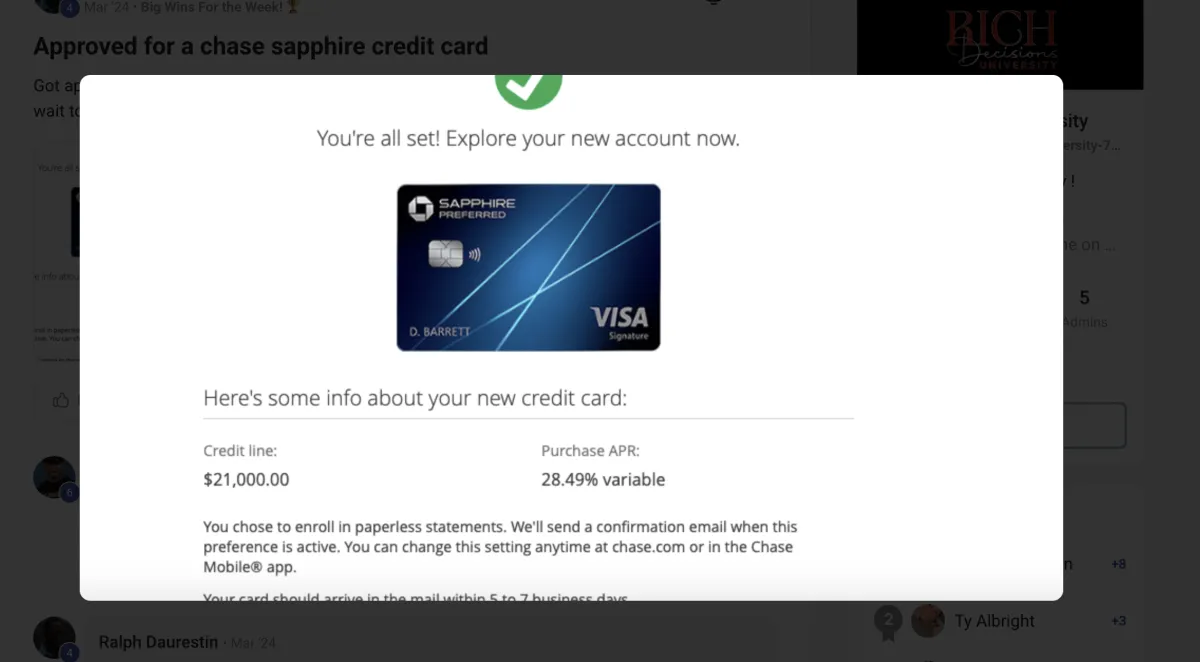

Banks don’t approve you based on your score alone.

You can have a 750+ credit score and still get denied.

Why? Because banks look at:

The types of accounts on your profile

The limit structure of those accounts

Your usage patterns, not just utilization

Your payment behavior over time

And how “bank-ready” your overall profile looks compared to other borrowers they approve

With Your Order Today

Unlock Immediate Access To

Are you fundable ebook

WITH The Credit Optimization Blueprint

Exact account mix banks want to see (not guesswork)

Proper utilization strategy (below 10–30%)

Primary tradeline structure explained

Payment history stacking method

90-Day profile optimization roadmap

WITHOUT The Blueprint (Why Most People Get Denied)

High utilization killing approval odds

Random accounts with no lending structure

700+ score but weak profile foundation

Thin file with low limit primaries

No strategic positioning before applying

High LIMIT APPROVAL FRAMEWORK

How I Leveraged One $20K Approval Into Bigger Limits

With The High Limit Approval System

● ✅ Comparable limit leverage strategy

● ✅ Bank matching method explained

● ✅ Internal risk positioning tactics

● ✅ Relationship-based approval strategy

● ✅ How to turn 1 approval into 3–5

Without It

● ❌ Stuck with $1,000–$3,000 starter cards

● ❌ No leverage strategy

● ❌ Applying blindly to random banks

● ❌ Multiple denials lowering score

● ❌ No understanding of internal bank tiers

INQUIRY & NEGATIVE ITEM STRATEGY

Reduce Profile Risk Before Applying

With The System

● ✅ How to analyze hard inquiries properly

● ✅ Smart dispute positioning (what works, what doesn’t)

● ✅ Timing strategy before funding

● ✅ Risk reduction before applications

● ✅ When to dispute vs when NOT to

Without It

● ❌ Applying with 8–12 recent inquiries

● ❌ Disputing incorrectly and hurting profile

● ❌ Triggering fraud alerts accidentally

● ❌ No understanding of FICO risk metrics

● ❌ Applying while profile is unstable

What The Perfect Credit Profile Teaches You

This ebook breaks down, step-by-step, how to structure your credit the way banks expect before you apply.

Inside, you’ll learn:

The Types of Accounts Banks Want to See

Not all accounts are treated equally.

I explain which accounts strengthen your profile and which ones quietly hold you back.

Primary vs. Authorized Accounts

When they help. When they don’t.

And how experienced funding mentors actually use them strategically.

Utilization Beyond the 30% Myth

Why “keep it under 30%” is incomplete advice and how banks interpret usage patterns differently than credit apps do.

Payment History That Actually Matters

Why how you pay is just as important as if you pay

Why High Scores Still Get Denied

And how to fix the missing pieces banks don’t tell you about.

How to Build Comparable Credit

So future lenders already see you as someone who qualifies for higher limits.

Who This Ebook Is For

This is for you if:

You’re tired of getting low limits

You’ve been denied despite having “good credit”

You want access to real capital to scale your business

You want to stop wasting inquiries and start applying with confidence

You’re ready to treat credit like a financial tool, not a mystery

Why People Get Denied

❌They Only Focus on the Score

They chase 750+… but ignore profile strength.

❌They Don’t Have Comparable Limits

You can’t jump from $1,500 cards to a $25,000 approval without proof of capacity.

❌Weak Account Mix

Too many small retail cards. Not enough strong primary accounts.

❌Poor Utilization Timing

Applying while balances report high. Wrong usage behavior before underwriting.

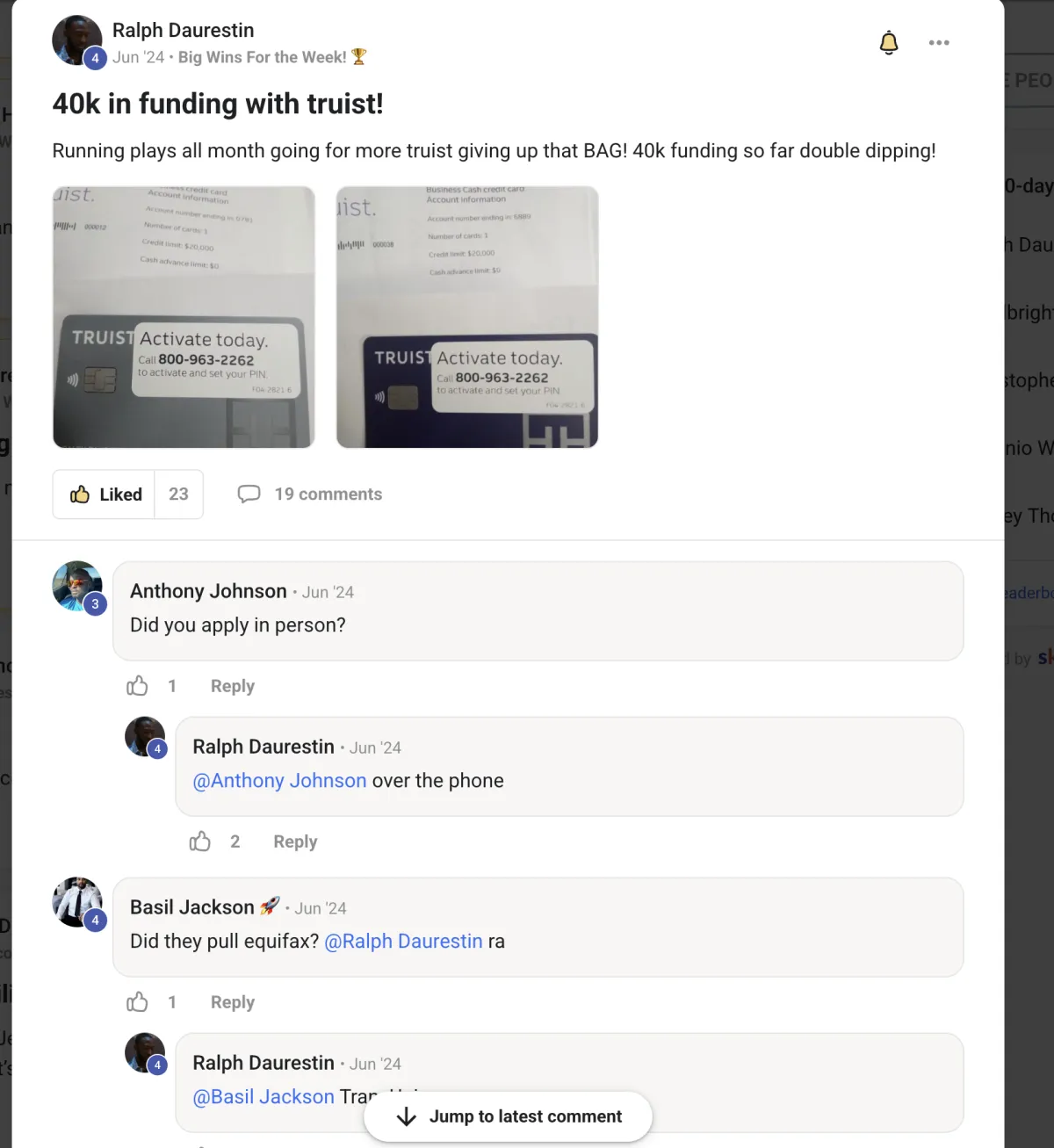

The approvals are real. The wins are real.

My peers are proof. It’s your move now.

You don’t want theory.

You don’t want motivation.

You want to know one thing:

If you're serious about accessing real funding — $20K, $50K, or more — this isn’t about your credit score.

If you're serious about accessIt’s about your profile structure.

This ebook breaks down:

✔ What banks actually look for

✔ Why 750 scores still get denied

✔ The exact accounts that make you fundable

✔ How to position yourself for stronger approvals

If you're tired of guessing…

And ready to structure your profile the right way…ing real funding — $20K, $50K, or more — this isn’t about your credit score.

FEATURE BREAKDOWN

A complete breakdown of the exact credit factors banks analyze before approving business funding — so you know precisely what to fix, optimize, and strengthen.

Most people focus only on their credit score, but banks don’t approve funding based on a number alone. They evaluate specific data points inside your credit profile — payment history, utilization ratios, credit age, account mix, comparable limits, recent inquiries, and overall profile thickness. Each of these factors carries weight in underwriting decisions, and if even one is structured incorrectly, it can reduce your approval odds significantly.

Inside this section, you’ll see a clear breakdown of how each feature impacts funding eligibility and what “approval-ready” actually looks like. Instead of guessing why applications get denied, you’ll understand the measurable standards lenders use to determine risk. When you know the exact criteria banks evaluate, you stop operating blindly — and start positioning your profile strategically for stronger approvals and higher limits.

Frequently Asked Questions

1. Is this just another credit repair ebook?

No. This is not a dispute-letter guide or a “boost your score fast” trick.

This ebook teaches you how to structure your credit profile the way banks actually approve high limits.

You can have a 750 score and still get denied. Why? Because banks approve based on profile structure — account types, limits, utilization, payment history, and depth — not just the number.

This book breaks down the exact structure lenders look for.

2. How fast will I see results?

That depends on your starting point.

If you already have strong primary accounts and clean payment history, you may be positioned for approvals much sooner.

If your profile needs optimization, this guide shows you exactly what to fix.

3. Can this help me access business funding?

Yes — and that’s the real goal.

Personal credit is the foundation for business funding. Once you understand how to build comparable limits and structure your profile correctly, you increase your chances of qualifying for higher approvals and stronger funding opportunities.

This ebook shows you how to position yourself before applying — not after getting denied.

Secure your Digital Copy Now!

Get your copy of the " Are you fundable" Ebook.

This site is not a part of the Facebook™ website or Facebook Inc. Additionally, This site is NOT endorsed by Facebook™ in any way. FACEBOOK™ is a trademark of FACEBOOK™, Inc.